The Federal Reserve Generated A Boom, Clumsily Contracted It, And Left Us With A Badly Broken System.

A decade ago, Americans found themselves living through the greatest economic downturn since the 1930s. In the time since, much ink has been spilled about it. What caused the Great Recession? Why was it so severe? Were the policy responses effective?

The real world is complicated. And simple stories tracing cause A to effect B always leave out meaningful details. Reasonable people might disagree about the significance of this or that contributing factor. But there should be some consensus on the big picture. In my view, any account of the Great Recession that omits the following three features is woefully incomplete.

-

The Great Recession was preceded by Federal Reserve monetary expansion.

The economy was overproducing in the years leading up to the Great Recession. We often talk about the housing bubble. But the overproduction can also be seen in the aggregate data. Capacity utilization increased from 75.63 percent in January 2003 to 79.91 percent in January 2007. Over the same period, labor force participation for those in their prime earning years (25-54) increased from 82.9 to 83.4 percent while the unemployment rate fell from 5.8 percent to 4.6 percent.

What caused the boom? There were many contributing factors. But, as the late Anna Schwartz observed at the time about booms in general, expansionary monetary policy usually plays an important role:

If you investigate individually the manias that the market has so dubbed over the years, in every case, it was expansive monetary policy that generated the boom in an asset. The particular asset varied from one boom to another. But the basic underlying propagator was too-easy monetary policy and too-low interest rates that induced ordinary people to say, well, it’s so cheap to acquire whatever is the object of desire in an asset boom, and go ahead and acquire that object.

In other words, poor monetary policy fueled an unsustainable boom.

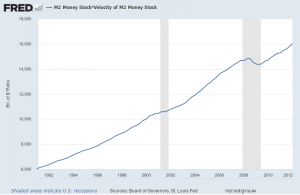

We can see this in the data. Ideally, the supply of money would be managed to offset any changes in the demand to hold it. Hence, the product of the money supply and the velocity of money (the latter of which is inversely related to the demand to hold money) should grow at a steady pace. From January 1991 to 2001, the product of M2 and velocity of M2 grew at a continuously compounding annual rate of roughly 5.50 percent. From January 2003 to 2007, it grew more rapidly, at a rate of 5.97 percent. Faster money growth relative to money demand fueled a boom.

-

The Great Recession was exacerbated by Federal Reserve monetary contraction.

When monetary expansion generates an unsustainable boom, a period of correction must follow. Resources, having been misallocated, must be reallocated. Machines will be repurposed, retooled, or relocated. Workers will spend time looking for new jobs, perhaps taking a break to gain new skills as well. And, all the while, the economy will be producing less.

But reallocation recessions tend to be small, roughly in proportion to the booms they follow. We cannot explain the biggest economic downturn since the Great Depression by pointing solely to the requisite reallocation. After all, the preceding overproduction was fairly modest.

Why, then, was the Great Recession so severe? In brief: monetary mismanagement. Having grown rapidly in the mid-2000s, the growth rate of M2 times velocity of M2 fell over the first three quarters of 2008 and then turned negative. The Fed allowed nominal spending to contract. And, since the price level does not adjust instantaneously, real output fell as well.

-

The Great Recession resulted in a radical change to the Federal Reserve’s conduct of monetary policy.

Perhaps least appreciated in all of this is the change in the Federal Reserve’s operating regime. Prior to the Great Recession, the Fed engaged in open market operations — largely limited to short-term Treasuries — in an effort to influence the effective federal funds rate. Since October 2008, the Fed has maintained a floor system, in which the interest it pays on reserves functions as the primary policy tool. The size of its balance sheet has exploded, and the composition has changed to include much riskier assets.

The Fed’s new operating regime is worse in several respects. First, maintaining a floor system requires setting the interest on reserves at or above the rate that would clear the federal funds market. That means monetary policy will tend to be tight on average, as the Fed fears setting the interest on reserve rate too low and seeing all of the new money it has created pour out into the economy.

Second, to maintain a larger balance sheet, the Fed must bid savings away from the private banking system. That reduces the extent to which valuable financial intermediation takes place and, correspondingly, the extent to which valuable investments and expenditures on research and development take place.

Third, since paying banks to hold reserves causes overnight-lending markets to dry up, banks no longer need to incur the costs to monitor one another. That means banks can take on excessive risks with little fear of reprisal.

Finally, the new operating regime has made the Fed more vulnerable to short-sighted political influence. It is hard to say precisely how much of the growth slowdown since the Great Recession can be attributed to the Fed’s new operating regime, but it almost certainly accounts for some of it.

Much like the Great Depression of the 1930s and the Great Inflation of the 1970s, the Great Recession of the 2000s shaped a generation of macro- and monetary economists. We can debate the details. But three things warrant widespread agreement. The Fed generated an unsustainable boom. It followed up with a severe monetary contraction. And it swapped out its traditional operating procedures for a new regime, reducing economic growth and increasing systemic risk in the process.

This article first appeared at AIER.