In June of 2019 basketball great Kevin Durant tore his Achilles tendon. In the words of the Wall Street Journal’s Ben Cohen, what Durant suffered was “basketball’s most devastating injury.” Despite this, Cohen goes on to write that in 2021, there “is nothing about Durant that suggests he is diminished in any way.”

Durant is back, and arguably playing better than ever. Keep in mind that before the injury he was playing at a Hall of Fame level, and that with the exception of LeBron James, he was arguably the best basketball player in the world.

Cohen quotes surgeon Robert Anderson as saying that an Achilles tear ‘”used to be the kiss of death,”’ but not anymore. Per Cohen, “Medicine changed over several decades. Science did too. Past results would not be indicative of Durant’s future performance.”

Please think about this. What used to end careers in basketball no longer necessarily does.

Notable about this is that all manner of maladies not related to sports used to amount to death sentences. As this column routinely makes plain, pneumonia used to be “Captain of Man’s Death” per the late surgeon and author, Lawrence D. Dorr. Tuberculosis was a quick life ender too. So was yellow fever. Cancer was a certain killer, but then most didn’t live long enough for some form of cancer to get them. See what used to bring on mortality first.

So what happened? Economic growth did. It’s that simple. Economic growth produced resources necessary for healthcare experimentation and advances that ultimately saved lives. Per Dorr, people could more and more “live once,” but “die twice.” As in people could survive what killed their ancestors, all care of medical advances made possible by the matching of the talented with the resources that are a consequence of economic growth. Wealth would save lives.

Crucial here is that wealth can’t be decreed, or engineered by governments despite what President Biden wants you to believe. Wealth is created. Always.

Which means that when politicians like Biden, and economists like Treasury secretary Yellen claim that a “big,” $1.9 trillion “stimulus” plan from the federal government will revive the U.S. economy, they’re lying. Through their teeth. There’s not a word in their confident pronouncements that has a kernel of truth to it. Government quite simply cannot create wealth. It can only redistribute wealth already created via its taxing and borrowing power, which means that Biden and Yellen’s confident pronouncements will ultimately amount to historical monuments to double counting. Government cannot create. It can only redistribute.

The only thing government can do is to get out of the way. The natural state of free people is to progress. To grow. If the aim is economic growth, the only answer is freedom for the individuals who comprise any economy to produce without limits foisted on them by witless politicians and economists.

Government spending is a certain limit placed on progress precisely because central planning doesn’t work. Since government can only redistribute previously created wealth with its spending, the latter signals the politicized allocation of what’s precious. It signals Nancy Pelosi, Chuck Schumer and Joe Biden substituting their judgement about how wealth should be allocated to the detriment of actual visionaries like Jeff Bezos, Elon Musk and Peter Thiel. Three individuals who have no track record when it comes to innovation or prescient investment, redistributing wealth that would otherwise be allocated in more careful, knowledgeable and market-driven fashion by some of the world’s greatest minds.

In short, government spending is by its very name an economic somnolent. The more wealth the federal government redistributes, the less that’s available for intrepid entrepreneurial endeavor without which there is no progress.

Back to Durant, medical and scientific advances have made it possible for athletes to come back from what used to end their careers. About those advances, they didn’t just happen. They were the direct result of brilliant medical and scientific minds being paired with wealth previously created.

This is why government spending is so dangerous. When governments spend, they consume wealth. Conversely, when the wealth creators in our midst get to keep the fruits of their enterprise, they have no choice but to put it to work. Translated, there are only so many houses, vacations, cars and other rich baubles that the well-to-do can buy. What they don’t spend builds the capital base, and with it capital available to the innovative.

About this, some will say government spends on research too. Sure it does. But implicit there is that absent politicized research, that it wouldn’t happen. Please. That’s not serious. Private investment is all about removing unease from our lives, including erasing diseases. In other words, if the federal government were a microscopic fraction of its present self, there would still be the internet, cancer cures and other remarkable advances. The only difference is that they likely would have come sooner thanks to politicians consuming exponentially less of the wealth always and everywhere created in the private sector first.

And what about the lockdowns? By their very name they were anti wealth creation. Workers and business owners suddenly saw their ability to create wealth curtailed. With less wealth created, there’s necessarily less progress. Lockdowns instituted with health in mind were logically anti-health precisely because they were anti-wealth. They were anti resource without which the creative can’t vivify what’s on their minds.

What will it mean for the future? Very simply, this tragic imposition of command-and-control by politicians means progress against career-ending injuries for athletes will likely slow, the discovery of what will eventually render the internet primitive will similarly be rendered a more distant object, and then progress against diseases that still kill us will have been relatively suffocated. All so politicians could “do something.”

This article, summarizing a National Bureau Of Economic Research working paper, is a bit technical but we present it to make a point. Many decry the excessive wealth of founder-innovators and CEO’s of today’s leading tech companies. But those executives and shareholders capture very little of the total value they create for customers. They are making us richer more than they are making themselves richer.

With the sharp rise in productivity growth over the last decade, economists have been curious about the extent to which the fruits of higher productivity are captured by innovating firms. Is the rapid technological change in the New Economy – with double-digit rates of productivity growth in computers and a phenomenal increase in new products and services via the Internet – leading to a similar rapid rise in the profits of New Economy firms?

In Schumpeterian Profits in the American Economy: Theory and Measurement (NBER Working Paper No. 10433), author William Nordhaus studies the impact of new technology on profits, emphasizing three important implications: first, understanding the role of innovational profits in total profits; second, identifying the impact of innovation in stock market returns; and third, gaining greater understanding of technology’s wealth effect on aggregate demand, as defined by Federal Reserve Chairman Alan Greenspan (an effect he labels the “Greenspan effect.”)

Nordhaus begins by considering the impact of technological change on prices and profits. Do technological improvements primarily result in lower prices for consumers or in higher profits for producers? If producers are able to capture (or appropriate) most of the social returns to innovation, then profits will rise and prices will fall relatively little.

How much of the profits from a new technology are captured by innovators will vary greatly across industries. For sectors where knowledge is in the public domain, such as weather forecasting, the new knowledge cannot be appropriated and productivity improvements are passed on in lower prices. In other industries with well-defined products and strong patents, such as pharmaceuticals, producers may be successful in capturing a large fraction of social gains in “Schumpeterian profits.”

Nordhaus begins by developing a model for explaining the size of Schumpeterian profits. In this context, Schumpeterian profits are profits above those that are associated with the normal return to investment and risk-taking. The Schumpeterian profit margin, defined as the ratio of Schumpeterian profits to total revenues, is determined by three parameters: the rate of innovation-driven total factor productivity; the instantaneous appropriability ratio; and the depreciation rate on Schumpeterian profits. The only novel parameter is the instantaneous appropriability ratio, which measures the fraction of the social surplus that is captured by the innovator in the first year. Depreciation is particularly important for Schumpeterian profits because they are often eroded by such factors as the expiration or non-enforcement of patents, the ability of competitors to imitate or to innovate around original innovations, and the introduction of superior goods and services.

Nordhaus presents a numerical example of the outcome of the model. If the rate of innovation-driven total factor productivity is 2 percent per year, the instantaneous appropriability ratio is 50 percent, and the depreciation rate on Schumpeterian profits is 10 percent per year, then Schumpeterian profits would be 2 percent of total sales. If the rate of profit on capital is 10 percent per year and the capital-output ratio is 2, then in this simple example, Schumpeterian profits would be half of the return to capital.

Another application of the model would be to the New Economy (computers, software, telecommunications, and similar industries). To what extent, he asks, did the phenomenal rise in the stock prices of New Economy firms in the late 1990s reflect rapid innovation and high appropriability in that sector. He suggests the following example: The new economy amounts to 5 percent of nominal output. Assume that, after 1995, costless productivity growth in this sector shot up from 5 percent per year to 15 percent per year. The new economy would then be adding about $75 billion in social surplus in the initial years. If the new entrepreneurs could capture 90 percent of the new economy surplus in Schumpeterian profits, then with other plausible parameters, the increase in value of new economy firms would be $6 trillion. This in fact is close to the increase in value of new economy firms from 1995-2000.

But is this parable plausible? For the entire postwar period and for the nonfarm business sector, Nordhaus estimates that innovators are able to capture about 2.2 percent of the total surplus from innovation. This figure results from an instantaneous appropriability estimated at 7 percent and a rate of depreciation of Schumpeterian profits of 20 percent per year. This number implies that Schumpeterian profits were 0.19 percent per year of the replacement cost of capital over the period 1948-2001.

Using these estimates for the New Economy suggests that entrepreneurs could capture only $400 billion, not $6 trillion. Nordhaus speculates that part of the New Economy bubble might have arisen because investors overestimated the appropriability of innovations in that sector. Indeed, there is some evidence that appropriability in New Economy sectors is even lower than in Old Economy sectors. The new economy’s industries are marked by easy entrance and exit: bright ideas were readily funded, but imitators are just as quick to follow. Additionally, information is expensive to produce but inexpensive to reproduce, a factor that will erode the value of intellectual property rights and reduce the durability of Schumpeterian profits in that sector.

Nordhaus next considers the role of Schumpeterian profits through the Greenspan effect, which Nordhaus defines as the impact of rising productivity on aggregate demand through the wealth effect on consumption. Nordhaus’s calculations suggest that the Greenspan effect on aggregate demand through consumption is about one-quarter of the effect on potential output. In other words, the impact of productivity growth on potential output is about three times the effect on aggregate demand.

These estimates of Schumpeterian profits may seem implausibly low, Nordhaus says, given the inventiveness of the American economy. But they do fit into one of the major puzzles of corporate America: Why is the rate of profit on corporate capital so low? The rate of profit after tax on non-financial corporations over the past 40 years has averaged 5.9 percent annually, which was very close to the cost of capital. How could the rate of profit be so low, considering that profits include so much (such as monopoly and Schumpeterian profits) and the denominator omits several important assets (such as land and intangible investments)? At least part of the answer lies in Nordhaus’s finding that only 20 basis points of the rate of return to capital were attributable to Schumpeterian profits.

Who are the drivers of prosperity? Economists would say it’s them. At least the ones who work for the Federal Reserve and the US Treasury and numerous think tanks and lobbying firms in Washington DC would say that. They capture economics in mathematical models, with variables like money supply, government spending, workforce participation, and mysterious forces like technological advance. By tweaking their variables, they believe they can forecast outputs such as GDP and employment levels. The economy is a mathematical machine and they are the geniuses in charge.

Bezos, Zuckerberg, and Cook would say it’s them. They run the tech companies that dominate global commerce, employ people, provide retail platforms for minion companies that sell apps and gadgets and groceries. Without them, there’d be no economy and no prosperity.

Larry Fink at BlackRock, Jamie Dimon at JPMorgan Chase, David Solomon at Goldman Sachs, Warren Buffet at Berkshire Hathaway, and the other titans of finance would say it’s them. They are the financial capitalists who supply the juice to keep the economic lights burning.

Prosperity on a national scale—mass flourishing—comes from broad involvement of people in the processes of innovation: the conception, development, and spread of new methods and products—indigenous innovation down to the grassroots. This dynamism may be narrowed or weakened by institutions arising from imperfect understanding or competing objectives. But institutions alone cannot create it. Broad dynamism must be fueled by the right values and not too diluted by other values.

Note the term “broad involvement”. Phelps means everyone in the nation: he describes a culture of innovation.

the stuff of flourishing—the change, challenge, and lifelong quest for originality, discovery, and making a difference.

Modern economies display what he calls dynamism: the appetite and capacity of “indigenous innovation”, and “original ideas born of creativity and grounded on the uniqueness of each person’s private knowledge, information and imagination”. Phelps is not an Austrian economist – he can’t afford to be, since he chooses to make his name and his living inside the academic fortress of Keynesianism, not assaulting it from the outside. But he certainly sounds like one in his invocation of subjectivity in identifying these personal, individual, and psychological drivers of prosperity.

There are great benefits for the individuals who populate and participate in a dynamic modern economy:

the mental stimulus, the problems to solve, the arrival of a new insight, and the rest. I have sought to convey an impression of the rich experience of working and living in such an economy. As I considered this vast canvas, I was excited to realize that no one had ever depicted what a modern economy felt like.

“What a modern economy felt like”! Isn’t that the ultimate in subjectivism in economics? He goes further into subjectivism by identifying attitudes and beliefs as the drivers of economic results.

attitudes and beliefs were the wellspring of the dynamism of the modern economies. It is mainly a culture protecting and inspiring individuality, imagination, understanding, and self-expression that drives a nation’s indigenous innovation.. (with) a new set of values – modern values like expressing creativity for its own sake, and personal growth for one’s own sake.

As measures of prosperity, Phelps focuses largely on survey data: people answering questions about how they feel. Among the most important of these, in Phelps’s mind, are job satisfaction scores and life satisfaction scores. He conducts a comparative analysis across (mostly Western) countries that leads him to conclude that people derive more life satisfaction from activities as producers than activities as consumers. This finding stands in opposition to many of the critics of capitalism, who deride the system for making conspicuous consumers of us all, focused on what we buy rather than what we make.

As producers, it is our individual knowledge that gives us power:

it would appear that only increasing economic knowledge—knowledge of how to produce and knowledge about what to produce—could have enabled the steep climb in national productivity and real wages in the take-off countries.

With time, the modernist emphasis on increasing knowledge—and the presumption that there is always more knowledge to come—triumphed over traditional emphases on capital, scale, commerce, and trade. But where did that knowledge come from? Whose “ingenuity” was it?

More satisfaction from non-material rewards than from material rewards;

An outsize desire for achieving something through one’s own efforts (and being recognized for it);

Huge satisfaction in succeeding and prospering;

Delight in the sense of flourishing that comes from life’s journey and the thrill of voyaging into the unknown;

Satisfaction from making a difference, making a mark.

Underlying these satisfactions are the values of individualism, vitalism, and self-expression. Modernist satisfactions are inherently individualistic: one’s own and one’s closest family. Vitalism looks to challenges and opportunities that contribute to the feeling of being alive. Self-expression is the imagination and creation of new things and new ways that enable an individual to reveal who they are. Mass flourishing occurs in a dynamic economy where these humanist values fuel the necessary desires and attitudes for innovation and growth.

Phelps fears (and presents data to support those fears) that these values are being eroded in today’s America. Opposing values are gaining ground. There is considerable dissatisfaction among many participants in the modern economy. There appears to be a falloff in the non-material rewards of work. Household surveys show losses in reported job satisfaction and life satisfaction. There is a loss in the sense of agency, of the experience of succeeding at something and the sense of voyaging into the unknown. Some sociologists point to a rising narcissism among young people that makes them self-indulgent. They place more value on trying to be someone than on trying to do something.

We may be losing the dynamism of indigenous innovation that leads to mass flourishing. Check your attitude.

Entrepreneurs refuse to accept the status quo. Their function is to create new economic value for their customers, and thereby to profit for themselves, both financially and psychically. They do this by introducing new products and services to the marketplace, designing and implementing new processes, adding value to others’ inventions by turning them into market-wide innovations, and offering new pleasures and satisfactions and solutions that no-one knew of or imagined.

The pursuit of new is a refusal to accept the status quo. That includes any and all existing market conditions and structures, any monopolistic incumbent firms, any regulatory barriers, any capital shortages, any “it can’t be done” pessimism.

We think of entrepreneurs in economic terms, market movers dealing in goods and services, taking dollars and cents in exchange. But the entrepreneurial mindset and the entrepreneurial process can be applied in many more contexts where the status quo requires a challenge and change is called for. Functional entrepreneurship is a process that can be described as a series of steps:

Development of entrepreneurial belief. An entrepreneur develops and continually adapts and polishes a belief about the status quo that no-one else holds. The belief is that the status quo is inadequate, wrong, or susceptible to improvement. For whom? For customers – i.e. not for the entrepreneur herself but for others. The status quo is under-serving others, and the entrepreneur is determined to fix that error. The entrepreneur, of course, expects to get something back in return, which could be psychic fulfillment (a sense of purpose and meaning from being the status quo buster) as well as profit (which is the financial signal to the entrepreneur to keep going). It all starts with dissatisfaction and the belief in the possibility of eliminating it.

Alignment with customers: As the entrepreneur develops the belief, she or he continuously aligns with (potential) customers. Am I getting this right? Does what I believe align with your preferences? If I change things in the way I am thinking, will you endorse the change? You are the customer, and you are my guide. You have the final decision.

Implementation: Given supportive feedback from customers (“the market”), the entrepreneur moves ahead with the new initiative – designing, building, and marketing it. It’s offered to the market as a value proposition (“I think you might like this – here’s why”). The market (i.e. customers) responds yes, no or conditionally (“I’d like it better if………). The entrepreneur receives the feedback, reshapes the value proposition and re-offers it until the customer confirms “Yes! That’s it!”

This mindset and the BAI process – Belief, Alignment, Implementation – can be applied not only in business but in any context or setting where there is dissatisfaction with the status quo on which an entrepreneur can build a belief and a customer can express a preference. As a result, we can imagine a wide range of fields in which the entrepreneurial mindset can be applied to society’s benefit.

Institutional Entrepreneurship

Many of the institutions in our society have reached all time lows of disrespect. Representative democracy is being widely questioned, and the institution of Congress has a very low approval rating (18% job approval – and moving lower – according to Gallup Poll in mid 2020). Also in the Gallup Poll, half of Americans revealed “somewhat negative” or “very negative” ratings of the federal government. We are losing confidence in our money, and the Federal Reserve, the institution charged with preserving its integrity and value, yet does the opposite. Similarly, we re losing respect for educational institutions that prefer to indoctrinate our children rather than educate them.

In all these instances, there are entrepreneurs who have developed the belief that they can bring improvements to a corroded status quo. Even democracy can be innovated. Or, alternatively, we could re-think the entire founding of the US. Entrepreneurs are the ones who initiate these changes.

Regulatory Entrepreneurship

Regulation is the context in which entrepreneurs work. The more thoughtful entrepreneurs question whether the context is unchangeable, and they find innovative ways to make change. Uber and AirBnB are recent multi-billion dollar examples of what’s possible. Uber is what contracted automobile transportation looks like when entrepreneurs question the regulation that keeps the restrictive taxi monopoly in place. According to Josh Johnston Airbnb is just what hotels look like without hotel regulations. Entrepreneurs can out-think regulators.

Social entrepreneurship

Social entrepreneurship is a term that is often misused to mean entrepreneurial initiatives that are conducted without a profit motive, aiming for a higher target of good for society that entrepreneurial capitalism can’t achieve. The true case is that all entrepreneurship is for social good, because society is simply another word for entrepreneurs’ customers, and entrepreneurs want them to do well. Entrepreneurs offer society more and more good things, while trying to use less and less of society’s resources (i.e. lower costs), thereby freeing them up for other social uses.

A great example of profit-directed social entrepreneurship is the initiative called Entrepreneur Zones, the brainchild of Dale Caldwell of Fairleigh Dickinson University’s Rothman Institute of Innovation and Entrepreneurship. With Entrepreneur Zones, Dr. Caldwell aims to solve problems of urban poverty, family instability and academic underachievement by establishing an environment where local residents can start and grow businesses and make them thrive, in n environment of shared purpose, supportive investment, training, mentoring and relaxed regulation. The goal is to improve society by making a profit, generating jobs, and creating the social environment in which families can pay their bills and their kids can do well in school.

Cultural Entrepreneurship

In November 2020, Frank Newport of Gallup wrote A Letter to Elected Representatives, From the Average American, based on what average Americans had told Gallup in surveys. One of the statements is this: “I have lost faith in many of our culture’s institutions in recent years”. The term cultural institutions can include many things from religion to the healthcare system. Gallup reports that Congress has by far the lowest confidence of all institutions, of course, but confidence in many of our other institutions is redoing too. The next lowest after Congress is big business followed by the news media (TV and Newspapers), the criminal justice system, and organized labor, then banks and public schools.

We can see entrepreneurial improvements emerging for all these institutions. Home schooling and private schools; fintech replacing many bank functions; reformers trying to change the criminal justice system; internet news outlets offering alternatives to mainstream news media. Consumers get to choose which of these innovations they’ll support. Entrepreneurs will continue trying to secure that support through integrity, earning trust, and giving great service, which is where so many of our institutions fail.

Entrepreneurs and entrepreneurship are society’s resources for continuous improvement of the status quo.

People are often afraid to go out on an entrepreneurial limb – but now’s a better time than ever to build a business. Recessions and unstable periods often present the best opportunities to start new companies. During the 2008 financial crisis, for example, startups like Uber, AirBnB and many others were founded partly as a response to changing market dynamics.

In a little-known challenge to the economic fallout of the pandemic, millions of people have turned the crisis into an opportunity for progress. That is especially true in the United States. According to the Census Bureau, new businesses are springing up at the fastest rate in more than a decade. So far in 2020, the bureau has received more than 3.2 million applications for employer identification numbers. The comparable figure for the same period last year was 2.7 million.

Faced with furloughs or layoffs, many people are fashioning their own form of work. They see the pandemic as a now-or-never time to pursue a dream. (See related story, here.) Choose your cliché to explain this burst of entrepreneurship: Necessity is the mother of invention. Sweet are the uses of adversity. If life gives you lemons...

Some people can obtain loans, but many start with their own savings, driven by the passion of a good idea to invest in a new service or product. They tap into unexplored creativity, flexibility, and adaptability. “The most important lesson of COVID-19 is learning to adapt,” Myriam Simpierre, who opened a neighborhood grocery in New York City, told MarketWatch. “Distribution channels go awry. Prices change. A pandemic happens. Anything can happen. You have to be adaptable.”

Another entrepreneur who opened a hair salon makes sure she regularly sweeps the sidewalk out front and provides a bowl of water for passing canines, giving her an opportunity to “talk to everybody” passing by. In turn, she says, the neighborhood has embraced her business.

While many existing businesses have been forced to shut down, optimistic newcomers push ahead, in part out of a joy in being their own boss. The pandemic has produced a supercharged version of “creative destruction,” the theory that a good economy thrives when older businesses lose their way and innovative ones spot an opening. That churn is also putting the lie to the idea that only big corporations will survive the pandemic.

One reason many of these new businesses are enjoying early success is that customers crave in-person buying experiences after long periods of social isolation. That’s especially true when customers can meet new people, such as in a cafe. Other entrepreneurs spot new trends – such as a strong demand for bicycles – that they can supply.

A personal trainer in Madison, Wisconsin, who lost his job, started a mobile bicycle repair business, investing about $1,000 in equipment. Now he’s booked fixing bikes at people’s homes all day long, earning more than he did in his previous job.

“It feels like I built a rocket and lit it – and now I’m just holding on to the tail,” he told The Wall Street Journal.

Starting a new venture can be scary. But it can also be liberating. People find they must draw on their innate qualities, such as a humility to serve or the courage to test a new idea. Those are the fuel behind any new venture and are just one of the salves during the pandemic.

This article first appeared at Christian Science Monitor (csmonitor.com)

This is a story about when big innovations happen.Not how, but when. And to some extent, why.Hopefully you find it counterintuitive at first before it quickly seems obvious. That’s how most important ideas work.And hopefully you’ll see why 2020, for all the hell its brought, could be the new beginnings of something promising.Cars and airplanes are two of the biggest innovations of modern times.

But there’s an interesting thing about their early years.

Few looked at early cars and said, “Oh, there’s a thing I can commute to work in.”

Few saw a plane and said, “Ah-ha, I can use that to get to my next vacation.”

What they did say early on was, “Can we mount a machine gun on that? Can we drop bombs out of it?”

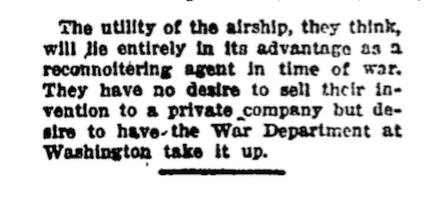

Every new invention looks like a toy at first. Adolphus Greely was one of the first people outside the car industry to realize the “horseless carriage” could be useful.

Greely, a brigadier general, purchased three cars in 1899 – almost a decade before Ford’s Model T – for the U.S. Army to experiment with. In one of its first mentions of automobiles, The Los Angeles Times wrote about General Greely’s purchase:

It can be used for the transportation of light artillery such as machine guns. It can be utilized for the carrying of equipment, ammunition and supplies; for taking the wounded to the rear, and, in general, for most of the purposes to which the power of mules and horses is now applied.

Nine years later, the LA Times did an interview with young brothers Wilbur and Orville Wright, who talked about the prospects of their new flying machine:

The Wrights had reason to believe this was true. Their only real customer in their early years – the only group to show interest in airplanes – was the U.S. Army, which purchased the first “flyer” in 1908.

The Army’s early interest in cars and planes wasn’t a fluke of lucky foresight. Go down the list of big innovations, and militaries show up repeatedly.

Radar.

Atomic energy.

The internet.

Microprocessors.

Jets.

Rockets.

Antibiotics.

Interstate highways.

Helicopters.

GPS.

Digital photography.

Microwave ovens.

Synthetic rubber.

They all either came directly from, or were heavily influenced by, the military.

Why?

Are militaries home to the greatest technical visionaries? The most talented engineers?

Perhaps.

But more importantly they’re home to Really Big Problems That Need to Be Solved Right Now.

Innovation is driven by incentives. And incentives come in many forms.

On one hand there’s, “If I don’t figure this out I might get fired.” That will get your brain in gear.

Then there’s, “If I figure this out I might help people and make a lot of money.” That will produce creative sparks.

Then there’s what militaries have dealt with: “If we don’t figure this out right now we’re all going to die and the world will be taken over by Adolf Hitler.” That will fuel the most incredible problem-solving and innovation in the shortest period of time that the world has ever seen.

The 1955 book The Big Change describes the burst of scientific progress that took place during World War II:

What the government, through its Office of Scientific Research and Development and other agencies, was constantly saying during the war was, in effect: “Is this discovery or that one of any possible war value? If so, then develop it and put it to use, and damn the expense!”

The result has been likened to a team of experts combing through a deskful of scientific papers, pulling out those which gave promise of usefulness, and then commandeering all the talent and appropriating all the money that might be needed to translate formulae into goods.

Militaries are engines of innovation because they occasionally deal with problems so important – so urgent, so vital – that money and manpower are removed as obstacles, and those involved collaborate in ways that are hard to emulate during calm times.

You cannot compare the incentives of Mountain View coders trying to get you to click on ads to Manhattan Project physicists trying to end a war that threatened the country’s existence. You can’t even compare their capabilities. The same people with the same intelligence have wildly different potential under different circumstances.

Militaries are an extreme example of panic-induced innovation.

A broader point that applies to everyone is that the biggest innovations rarely occur when everyone’s happy and safe, or when the future looks bright. They happen when people are a little panicked, worried, and when the consequences of not acting quickly are too painful to bear.

That’s when the magic happens.

The 1930s were a disaster.

Almost a quarter of Americans were out of work in 1932. The stock market fell 89%.

Those two economic stories dominate the decade’s attention, and they should.

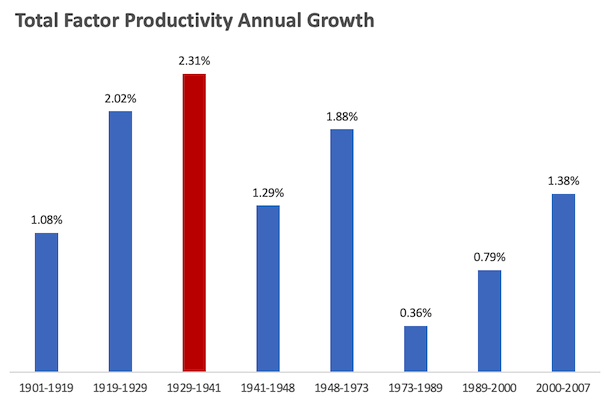

But there’s another story about the 1930s that rarely gets mentioned: It was, by far, the productive and technologically progressive decade in history.

The number of problems people solved, and the ways they discovered how to build stuff more efficiently, is a forgotten story of the ‘30s that helps explain a lot of why the rest of the 20th century was so prosperous.

Here are the numbers: Measuring total factor productivity – that’s economic output relative to the number of hours people worked and the amount of money invested in the economy – hit levels not seen before or since:

Economist Alex Field writes:

In 1941, the U.S. economy produced almost 40 percent more output than it had in 1929, with virtually no increase in labor hours or private-sector capital input. Almost all of the increase in output per hour is attributable to technological and organizational advance [of the 1930s].

A couple of things happened during this period that are worth paying attention to, because they explain why this happened when it did.

The New Deal’s goal was to keep people employed at any cost. But it did a few things that, perhaps unforeseen, become long-term economic fuels.

Take cars. The 1920s were the era of the automobile. The number of cars on the road in America jumped from one million in 1912 to 29 million by 1929.

But roads were a different story. Cars were sold in the 1920s faster than roads were built. A new car’s novelty was amazing, but its usefulness was limited.

That changed in the 1930s when road construction, driven by the New Deal’s Public Works Administration, took off.

Spending on road construction went from 2% of GDP in 1920 to over 6% in 1933 (vs. less than 1% today). The Department of Highway Transportation tells a story of how quickly projects began:

Construction began on August 5, 1933, in Utah on the first highway project under the act. By August 1934, 16,330 miles of new roadway projects were completed.

Historian Robert Grodon writes:

The 1930s witnessed the construction of multilane engineering marvels, including the George Washington, Golden Gate, and Bay Bridges, as well as the beginning of multilane limited-access turnpikes, including the Merritt Parkway in southern Connecticut and the first section of the Pennsylvania Turnpike. These anticipated, and in some cases became part of, the postwar Interstate Highway System. As of 1940, a map of the principal routes of the U.S. highway system looks virtually identical to a map of today’s Interstate Highway System, except that most of the roads were two-lane with intersections rather than featuring limited access.

The Pennsylvania Turnpike, as one example, cut travel times between Pittsburgh and Harrisburg by 70%. The Golden Gate Bridge opened up Marin County, which has previously been accessible from San Francisco by ferry boat.

Multiply those kinds of leaps across the nation and 1930s was the decade that transportation truly blossomed in the United States. It was the last link that made the century-old railroad network truly efficient, creating last-mile service that connected the world. A huge economic boon.

Electrification also surged in the 1930s, particularly to rural Americans left out of the urban electrification of the 1920s. The New Deal’s Rural Electrification Administration brought power to farms in what may have been the decade’s only positive development in regions that were economically devastated. The number of rural American homes with electricity rose from less than 10% in 1935 to nearly 50% by 1945.

It is hard to fathom, but it was not long ago – during some of our lifetimes and most of our grandparents’ – that a substantial portion of America was literally dark. Franklin Roosevelt said during a speech on the REA:

Electricity is no longer a luxury. It is a definite necessity. It lights our homes, our places of work and our streets. It turns the wheels of most of our transportation and our factories. In our homes it serves not only for light, but it can become the willing servant of the family in countless ways. It can relieve the drudgery of the housewife and lift the great burden off the shoulders of the hardworking farmer.

I say “can become” because we are most certainly backward in the use of electricity in our American homes and on our farms. In Canada the average home uses twice as much electric power per family as we do in the United States.

Electricity becoming a “willing servant,” – introducing washing machines, vacuum cleaners, and refrigerators – freed up hours of household labor in a way that let female workforce participation rise. It’s a trend that lasted more than half a century and is a key driver of both 20th century growth and gender equality.

A second productivity surge of the 1930s came from everyday people forced by necessity to find more bang for their buck.

The first supermarket opened in 1930. The traditional way of purchasing food was to walk from your butcher, who served you from behind a counter, to the bakery, who served you from behind a counter, to a produce stand, who took your order. Combining everything under one roof and making customers pick it from the shelves themselves was a way to make the economics of selling food work during a time when a quarter of the nation was unemployed.

Laundrymats were also invented in the 1930s after sales of individual washing machines fell – they marketed themselves as washing machine rentals.

Factories of all kinds looked at bludgeoned sales and said, “What must we do to survive?” The answer was often to build the kind of assembly line Henry Ford introduced to the world in the previous decade.

Output per hour in factories had grown 21% during the 1920s. “During the Depression decade of 1930-1940 – when many plants were shut down or working part time” historian Frederick Lewis Allen writes, “there was intense pressure for efficiency and economy – it had increased by an amazing 41 per cent.”

He wrote again in 1943:

Anybody can understand the basic principle of a fork truck. But the layman can only stand in awe before some of the complex electronic machines which came into use after 1935 – machines for measuring materials with microscopic exactitude, or for watching the performance of a machine and automatically correcting flaws in its performance. The language used by engineers in talking about them is quite unintelligible to him, as are the processes involved. But at least he can appreciate the miraculous results they achieve.

Something as simple as quality control sampling massively reduced manufacturing waste and became common in the 1930s. Lewis Allen again:

The workman can thereupon regulate the adjustment of his machine, not by guesswork, but with exact knowledge of just how it is functioning. This [process] – which in many a factory has saved large amounts of money by reducing the number of defective products – has the effect of raising the status of the workman by making him in a special sense his own boss, the informed critic and judge of his performance.

This story was repeated across industries. Productivity growth in the 1930s was not constrained to a few fields, like it was in the 1920s when manufacturing accounted for nearly all the gains. The ‘30s saw huge technical progress in utilities, farming, wholesale trade, retail, transportation, mining, and communication.

“The trauma of the Great Depression did not slow down the American invention machine,” Alex Field writes. “If anything, the pace of innovation picked up.”

Economist David Henderson writes:

“Topping” techniques in electricity generation — using exhaust steam from high-pressure boilers to heat lower-pressure boilers — raised capacity by 40 to 90 percent with virtually no increase in the cost of fuel or labor.

New treatments increased the life of railroad ties “from eight to twenty years.”

With new paints, the time for paint to dry on cars fell from three weeks (!) to a few hours.

[Total research and development] employment in 1940 was 27,777, up from 10,918 in 1933.

Driving knowledge work in the ‘30s was the fact that more young people stayed in school because they had nothing else to do. High school graduation surged during the depression to levels not seen again until the 1960s, according to Field. One student recalled:

High schools had a larger attendance than ever before, especially in the upper grades, because there were few jobs to tempt anyone away. Likewise college graduates who could afford to go on to graduate school were continuing their studies – after a hopeless hunt for jobs – rather than be idle.

All of this – the better factories, the new ideas, the educated workers – became vital in 1941 when America entered the war and became the Allied manufacturing engine.

The big question is whether the big technical leap of the 1930s could have happened without the devastation of the depression. And I think the answer is “no” – at least not to the extent that it occurred.

You could never push through something like the New Deal without an economy so wrecked that people were desperate to try anything to fix it.

It’s doubtful that business owners and entrepreneurs would have so urgently found new efficiencies without the record threat of business failure.

Managers looking at their employees and saying, “Go try something new. Blow Up the playbook, I don’t care,” is not something that gets said when the economy is booming and the outlook is bright.

Big, fast, changes only happen when they’re forced by necessity.

World War II began on horseback in 1939 and ended with nuclear fission in 1945. NASA was created in 1958 two weeks after the Soviets launched Sputnik and landed on the moon just 11 years later. Stuff like that rarely happens that fast without fear as a motivator.

It reminds me of this:

HOBBES: Do you have an idea for your story yet?

CALVIN: You can’t just turn on creativity like a faucet. You have to be in the right mood.

HOBBES: What mood would that be?

CALVIN: Last-minute panic.

There’s an obvious limit to stress-induced innovation.

There’s a delicate balance between the economy being thrown upside down, everyone inside it driven into action by necessary panic, while the foundations of the economy itself remain intact, capable of supporting the new ideas and innovations.

My guess is that balance has only happened a few times in modern history.

One was the period from 1930 to 1945. Parts of the Cold War might qualify, though it was concentrated in a few defense sectors.

Then there’s 2020.

The hardest thing about stress-induced innovation is reconciling that positive long-term trends can be born when people are suffering the most. It makes the topic difficult to even discuss without looking insensitive.

But think of what’s happening in biotech right now. Many have pessimistically noted that the fastest a vaccine has ever been created is four years. But we’ve also never had a new virus genome sequenced and published online within days of discovering it, like we did with Covid-19. We’ve never built seven vaccine manufacturing plants when we know six of them won’t be needed, because we want to make sure one of them can be operational as soon as possible for whatever kind of vaccine we happen to discover. We’ve never had so many biotech companies drop everything to find a solution to one virus. It’s as close to a Manhattan Project as we’ve seen since the 1940s.

And what could come from that besides a Covid vaccine?

New medical discoveries? New manufacturing and distribution methods? Newfound respect for science and medicine?

So many important discoveries happen by accident when frantic experimentation uncovers an unrelated quirk of science. In his book How We Got to Now, Steven Johnson writes:

Innovations usually begin life with an attempt to solve a specific problem, but once they get into circulation, they end up triggering other changes that would have been extremely difficult to predict … An innovation, or cluster of innovations, in one field ends up triggering changes that seem to belong to a different domain altogether.

This is happening in medicine right now. It’s happening with doctors in hospitals and scientists in labs. It’s impossible to know what it will lead to. But there’s currently so much experimentation, with stakes so high, that you know we’re going to look back in 10 or 20 years at the important discoveries that wouldn’t have been possible without Covid-19. That’s always how it’s worked.

Or think about cities.

I don’t think San Francisco or New York are dead – that’s absurd. But it doesn’t take many companies letting their employees work remotely to take the pressure off one of the biggest social problems of the last generation: affordable housing.

Having so much of the economy’s economic potential clustered in a few cities – a few neighborhoods, really – created $2 million starter homes in cities with good jobs and cheap homes in cities with little economic growth. Even a slight shift to permanent remote work could make cities more livable and rural areas more prosperous.

Or colleges. Student loans are another major social issue of the last generation. Without Covid the college industry would have likely corrected in the coming decades. With Covid it’s correcting in the coming weeks.

When schools say, “Pay full tuition and we’ll teach you over Zoom,” and students and parents say, “Wait, there’s no way that’s worth it,” you realize – quickly, in stark terms – that you’re not paying for an education. You’re paying for a credential and a social experience, which doesn’t need to cost $68,000 a year.

There’s a recognition that education — the value, the price, the product — has fundamentally shifted. The value of education has been substantially degraded. There’s the education certification and then there’s the experience part of college. The experience part of it is down to zero, and the education part has been dramatically reduced. You get a degree that, over time, will be reduced in value as we realize it’s not the same to be a graduate of a liberal-arts college if you never went to campus. You can see already how students and their parents are responding.

It’s not crazy to say that could be the most important developments of the next generation, because student loans have been one of the biggest burdens of the past generation.

On the tech front, Microsoft CEO Satya Nadella said “two years of digital transformation took place in two months,” this spring.

What does that lead to?

Almost every business in the world is now asking how they can work more efficiently, save a few bucks here and here, and do more of their business online.

What does that lead to?

Tens of millions of people who lost their jobs, and hundreds of millions of people who kept theirs but worried, will be permanently scarred into thinking about risk, opportunity, and safety nets differently than they were six months ago.

What does that lead to?

I don’t think anyone knows the answers.

All we know is that the most important changes of the last 100 years have taken place during upheavals. And we’re currently in the biggest upheaval of the last 100 years.

We know that creativity and discovery surge when people are forced to find, rather than just want, new solutions.

We know that an irony of technology is that economies often make their greatest leaps forward when the outlook is bleakest.

It might be one of the only silver linings of 2020.

In October, 1933 an Ohio lawyer named Benjamin Roth wrote a diary entry about the economic carnage devastating his town. A quarter of the town was unemployed. Farms were bankrupt. Surviving businesses used new efficiencies to get by with fewer workers, exacerbating unemployment.

Roth tried to remain optimistic.

“I am confident that new inventions and scientific discoveries will remedy this situation,” he wrote.

At nearly the same time he was writing an electrical engineer named Edwin Armstrong introduced a new radio technology to David Sarnoff, an RCA executive struggling to hold together an industry smashed by the Depression.

Sarnoff later recalled the conversation, as told in the book Man of High Fidelity:

“Why are you pushing this so hard?” asked Sarnoff.

“There is a depression on,” said Armstrong. “The radio industry needs something to put life in it. I think this is it.”

The technology – FM radio – transformed 20th century communication.

There’s a famous story of a Canadian inventor who developed an inexplicably fuel-efficient carburetor. Men from the oil industry reached out to him. The inventor soon disappeared and he and his carburetor were ultimately never seen or heard from again.

The story is of course patently bogus. Countless variations of it have been told since the early 20th century. The only remarkable part of the story is that it is inspired by a real Canadian inventor, Charles Nelson Pogue, who developed some patents that in no way shape or form paved the way for miraculous gains in fuel efficiency.

Still, it’s highly instructive that this has become an enduring urban legend. After all, an erudite lecture from the late Harvard professor Calestous Juma on “innovation and its enemies” is going to demand a lot more cognitive load. In lieu of that lecture, the urban legend of the miracle carburetor gets the same point across just fine; powerful interests do not always profit from technology getting better and faster.

In professor Juma’s 2016 tour de force historical overview of the various factions and socio-economic forces that impede innovation, he exposes the unholy alliance that often forms between “incumbent” firms on the one hand, and governments and reigning legacy institutions on the other. Juma provides a simple and obvious reason for this alliance: Governments, major media outlets, and other leading institutions obtain the lion’s share of their revenue from monopolistic incumbent firms. Hence, those institutions use regulations, propaganda, and other choice strategies to support incumbent firms, and sabotage iconoclastic entrepreneurs.

The illiberal anti-free expression philosophy that has taken hold across major American institutions is almost certainly a manifestation of those institutions underlying incentives to control innovation. Trying to crush innovative efforts on an ad-hoc, case-by-case basis is tiresome stuff. The US government hasn’t had much luck trying to shut down bitcoin. It’s far more effective to foster an environment with salient cultural restrictions on creativity and inquiry. That way, with a bit of luck, tyrants needn’t worry about blockchain coming into existence in the first place.

The authoritarian excesses of cancel culture cannot be divorced from the deep incentives felt by status quo industries and institutions. The idea that American institutions have been taken over by a principled left-wing ideology, championed by a mob of ideologues, is a misread of the actual situation. Indeed, there is rigorous documentation that American universities as prestigious as Yale are sacking professors who’ve voiced opinions (in jest) that raised the ire of conservatives.

A thorough review of the data on professors who were fired and demoted, over things that they said, confirms that many of them strayed too far to the left of the status quo. The reality of cancel culture is that anyone who offends enough people, or powerful enough people, is putting their career in jeopardy. Certainly, public outrage is a key component of cancel culture. With that said, the leaders of contemporary industries and institutions bear no undue burden on account of rank-and-file folks enabling their unforgiving despotism.

Principled ideology does not underlie the illiberal dysfunction in contemporary institutions. The underlying reasons are far crasser. Major institutions, and the oligopolies that fund them, have a vested interest in keeping a lid on free thought and free expression, simply to preserve the status quo. The highest ranking members of these organizations feel insecure in the face of technical and scientific change. Our current leaders don’t want to find themselves departing for anachronism and obscurity like the Catholic Church and European Nobility two centuries ago.

Industries’ Double-Edged Sword

Authorities like Oxford Martin and the International Monetary Fund have raised concerns about the current ability of monopolistic firms to suppress innovation. Top firms have achieved unprecedented market power in recent decades. Such firms can erect barriers to entry and horde assets like intellectual property, in order to thwart their emerging competitors. The Atlantic and The Verge have brought these concerns before a popular audience.

Lobbying for regulations that block disruptive entrepreneurs is an effective strategy favored by incumbent firms. In the late 19th century, American butter manufacturers successfully lobbied for anti-margarine laws. Cell phones would have been rolled out decades earlier if not for the radio spectrum being restricted, thanks to the lobbying efforts of broadcasters and radio common carriers. Tobacco interests have successfully lobbied against e-cigarettes. Academic research shows that top firms have obtained a healthy return on investment from lobbying and regulations, especially since the 2000s.

Another preferred method for fighting innovation is the use of propaganda. American Express has promoted an outlandish claim that cryptocurrencies are particularly bad for the environment. Thomas Edison famously went to extravagant lengths to make alternating current look dangerous and impractical since he was invested in direct current. Edison’s propaganda campaign included such macabre aspects as electrocuting dogs with alternating current and promoting its use for capital punishment.

It’s ironic because years earlier Edison had to jump through untold political hoops to introduce electric lighting to New York City and overthrow the incumbent—and less efficient—gas lighting industry. However, Edison’s hypocritical actions later in life are consistent with a rational decision-maker following the profit motive. The truth is that innovation is an industry’s double-edged sword; it’s good when it helps your bottom line and bad when it replaces your product line.

Thomas Edison’s meta-strategy is still being employed by Sir James Dyson. Dyson fought a five year legal battle against the EU because Europe’s mandatory energy efficiency tests were set up to make Dyson vacuums look less efficient than the competition. The competition—established German vacuum manufacturers—had lobbied for tests that were essentially rigged in their favor. Aside from those heroics, Dyson has funded credulous research that suited his company’s interests. This was in the context of an ongoing cutthroat PR war between Dyson and the respective manufacturers of paper towels and standard hot-air dryers.

Naturally, Dyson has promoted the company’s patented jet air dryer as the most hygienic and environmentally friendly way for a person to clean their hands. The other two factions responded in kind by promoting their own self-serving narratives. All three factions have funded scientific studies with a suspicious tendency to return results that suit the best interest of the funder. One major study with bona fide independent funding determined that paper towel was the most hygienic hand drying method. Of course, Dyson has funded research that promoted its jet air dryer.

Incumbent firms may not even be especially keen to test the limits of their own innovative prowess. Bell Labs suppressed the recording technology that they developed in the early 1930s. Senior management correctly assumed that such technology would have profound ramifications for society. However, they were being quite paranoid in thinking that people would stop using telephones because of it. These days, firms purposely design technology so that it stops working or at least loses some functionality by a predetermined date. This practice of planned obsolescence is considered a best practice.

The upshot is that monopolistic firms have a vested interest in controlling the wild world of pure research. There’s literally no telling what curiosity-driven research will produce next; it could just as easily bless or smite a given corporation. Industries are compelled to exercise control over the double-edged sword that is innovation.

Unholy Alliance vs. Double-Edged Sword

Innovation is the raison d’être for universities. But not unlike Bell Labs—the birthplace of C++, the transistor, and Unix—universities can’t be expected to be entirely gung-ho about innovation. The university’s shift to authoritarianism stems from fear of a world turned upside down by tech start-ups that don’t care about traditional higher education, and enumerable manifestations of open source. This existential uncertainty strengthens the natural partnership between universities and incumbent oligopolies.

It’s very important to note that the oligarch-institutions alliance will not benefit from a zero growth, zero innovation regime. Unlike ancient kings and priests, their power isn’t predicated upon simply maintaining peace and order. Their success hinges on innovation and growth, and yet, they need growth that they can control.

That’s not to say that the struggling masses would benefit from uncontrolled innovation. The atomic bomb, climate change, mass surveillance, and unclean air all came out of innovation. Innovation is a double-edged sword no matter who wields it, and so whoever takes up that blade must do so with a sense of control and skill. Does this mean that the oligarch-institutions alliance is simply serving its purpose in a functionalist sense?

The age of COVID-19 rips that pretense apart. Humanity cannot afford the sort of antics Dyson engaged in, commissioning research that purposely distracts from the public health risk of blasting aerosolized pathogens all over a washroom. Humanity cannot afford health organizations that dodge important questions, nor ones that give incorrect advice only to retract it after the damage is done. It’s important to note, the symbiotic relationship between powerful corporations that may have a conflict of interest with the facts, and institutions that do a poor job of finding and conveying the facts.

Miraculously, there is hope for innovation. The internet has allowed for the creation of a new intellectual ecosystem that champions innovation. The internet provides a perfect space to leverage the wisdom of the crowd and hash out a solution. What is certain is that we need to fight for a free and open internet, and keep pushing for revolutionary technologies—like blockchain—that empower people.

William Tomos Edwards is a writer, philosopher, and the founder of Bright Tapestry Data. This article first appeared at fee.org.

Entrepreneurship is the intentional pursuit of value. This pursuit fuels the engine of economic growth. The entrepreneurs who achieve the realization of value become folk heroes, and the great firms that create value at scale – Apple, Microsoft, Amazon, Facebook, Google – are stock market heroes.

All of this is acceptable wisdom. However, it’s the wisdom of outcomes, of recording the score after the play has been completed. Who drew up the play? Don’t we concede some genius to the coach and the offensive co-ordinator as well as the quarterback and the wide receiver?

Who Is Pursuing Value?

In order to understand cause and effect, we have to start at the input, not the outcome. Who is actually pursuing value? How did the entrepreneur – or Apple – know that something new was needed? That some improvement was required to retain the role of stock market hero?

Henry Ford is often quoted as saying (although he probably didn’t), “If I had asked people what they wanted, they would have said faster horses.” The implication is that he placed no faith in the identification of consumer needs. His preferred method was invention (coming up with something new through his own genius) followed by innovation (translating the invention into something that could be produced, and then sold on the market).

In fact, Ford’s attitude, according to Harvard Business Review, “had a very costly and negative impact on the Ford Motor Company’s investors, employees, and customers”. Because it turned out that, once consumers had Model T’s, they quickly decided that what they wanted was better cars. General Motors developed a response in the form of their “A Car for Every Purse and Purpose,” strategy which aimed to produce cars for distinct market segments aided by installment selling, used car trade-ins, closed car models, and annual model changes. The Ford Motor Company was quickly relegated to a minor, small-share role in the American automobile market.

Think of this as the genius of the consumer. One minute, they don’t have cars. Next minute they are demanding not only better cars, but also better ways to buy them, better aesthetics, greater variety and frequent upgrades. Such boldness, such expansive thinking, such imagination! Edison brought them lightbulbs, and they imagined a world of devices attached to an electricity grid providing on-call productivity services of all kinds. Steve Jobs brought them the iPhone and they interconnected themselves to each other and to sources of knowledge and to global supply chains.

The double genius of the consumer.

What is this genius? It is twofold.

First, it is consumers who actually create value. How so? Because they are the ones pursuing it. Entrepreneurs and the innovators put resources – such as cars and refined gasoline and silicon chips and touchscreens and internet connections – into consumers’ hands, and then the consumers roar into action, their creativity unleashed by new affordances. They try to create as much value as they can with the new resources. They drive to work and drive to school and drive across America and put grocery and tools in the backs of their cars (Hey, Henry! Make me a pick-up truck!), and maybe sleep in the car (Hey, Henry! Make me an RV!) and maybe make music in the car by singing and whistling to themselves or to their kids in the back seat (Hey, Henry! Where is the radio?), and maybe find themselves wishing they could call home to say when they’ll be home for dinner (Hey, Henry! How about a carphone?). Value occurs entirely in the consumer’s domain (or the customer’s if you are in B2B). Value is a feeling of satisfaction in the consumer’s mind.

Which brings us to the second aspect of the consumer’s genius. It’s their dissatisfaction. Henry Ford wanted to accuse them of lacking imagination. He got it all wrong. Anyone can imagine the future (flying cars for example). Not many can get it right. Consumers don’t waste their time on such high error rate activities. They concentrate on a subject where they are always right: their own feelings of dissatisfaction. “Henry, we get wet driving your car in the rain!” “Henry, it’s really hard to change the tires.” “Henry, I can’t afford to pay you that amount of money all at once. Give me some time, won’t you?” “You said it only comes in black, but blue is my favorite color.”“Henry, your Model T looks the same this year as it did last year.” “Henry, can you speed this thing up?” “Henry, I need to work remotely. Can you make my F150 like a mobile office?”

The consumer has big dreams.

How genius is this? Dissatisfaction indicates that the consumer is able to dream bigger than the producer. Every new invention that becomes an innovation and is introduced to the market is immediately scrutinized under the lens of dissatisfaction, critiqued and criticized. No matter how many millions or billions of development dollars went into it, no matter how many Ph.D. engineers and Harvard MBA’s brought it to market, it can not survive the consumer’s examination unimproved. Because the consumer has big dreams.

The genius of the consumer outstrips that of the entrepreneur. Economists see the entrepreneurial process as one of trial and error, with the emphasis on error – a lot of mistakes before arriving (with the help of consumer feedback, of course) at a salable proposition, which is defined as one that generates less dissatisfaction than some alternative on which the consumer could spend their money.

Entrepreneurs are still heroes of course. If they weren’t willing to invest time, money and ego into the process of trying to please consumers, despite all the rejections, then there would be no progress. We might still be driving Model T’s, because no entrepreneur was willing to suffer the wrath of dissatisfied customers. We love our entrepreneurs. And we especially love those with more empathy – more ability to listen to consumers’ complaints to stimulate their imaginations for future betterment.

But let’s not err in identifying the locus of genius in this market process. Let’s help consumers achieve their dreams (before those of the entrepreneur).

Modern society looks increasingly to government for protection from major crises, whether recessions, public-health disasters or, as today, a painful combination of both. Such rescues have their place, and few would deny that the Covid-19 pandemic called for dramatic intervention. But there is a downside to this reflex to intervene, which has become more automatic over the past four decades. Our growing intolerance for economic risk and loss is undermining the natural resilience of capitalism and now threatens its very survival.

The world economy went into this pandemic vulnerable to another financial crisis precisely because it had already become so fragile, so heavily dependent on constant government help. Governments have offered increasingly easy credit and generous bailouts not only to soften the impact of every crisis since the 1980s but also to try to boost growth during the good times.

Now, amid the worst crisis since World War II, governments are riding to the rescue again. In the U.S., the Treasury is adding trillions in automatic crisis spending (such as benefits for the unemployed) and discretionary spending (like cash payments to single jobholders making up to $99,000). The Federal Reserve is doing its part by cutting rates, printing massive amounts of new money and directly buying the debt of troubled companies for the first time.

The governments of many other countries are, likewise, launching an array of stimulus measures that would have been unimaginable a few months ago. The mantra of government officials is that these efforts are not only necessary but also will carry no cost or consequences. They believe that they can easily borrow to pay for it all because the last four decades of easy money have brought interest rates to near or less than zero: Money is free.

This is a dangerous form of denial. A growing body of research shows that constant government stimulus has been a major contributor to many of modern capitalism’s most glaring ills. Easy money fuels the rise of giant firms and, along with crisis bailouts, keeps alive heavily indebted “zombie” firms at the expense of startups, which typically drive innovation. All of this leads to low productivity—the prime contributor to the slowdown in economic growth and a shrinking of the pie for everyone.

At the same time, easy money has juiced up the value of stocks, bonds and other financial assets, which benefits mainly the rich, inflaming social resentment over growing inequalities in income and wealth. It should not be surprising that millennials and Gen Z are growing disillusioned with this distorted form of capitalism and say that they prefer socialism. The irony is that the rising culture of government dependence is, in fact, a form of socialism—for the rich and powerful.

What capitalism urgently needs is a new, more focused approach to government intervention—one that will ease the pain of disasters but leave economies free to grow on their own after the crises pass.

In the early 1980s, central banks started to win the “war” on double-digit inflation. Containing consumer prices allowed them to start pushing interest rates downward, at a time when financial deregulation was easing lending conditions and corporate bailouts were becoming standard practice.

The Fed intervened in the markets to counter the crash of 1987 and in 1998 organized the rescue of a specific financial firm, Long Term Capital Management, for the first time. In 2008 the Treasury stepped in to save an entire sector—banks at the core of the mortgage crisis—with $200 billion. Unable to do much more to cut rates, which were already close to zero, the Fed launched its first experiments in “quantitative easing,” buying up to tens of billions of dollars in assets each day, including mortgage-backed securities, to calm the credit markets.

The rest of the world followed the Fed. As interest rates fell toward zero, the world’s debts—including households, governments and nonfinancial companies—more than tripled between 1980 and 2007 to more than three times the size of the global economy. It was taking more debt to fuel the same amount of growth, because more debt was going to unproductive borrowers. Capitalism was bogging down.

Worldwide, recessions were decreasing in frequency and severity. In the 2010s, as easy money continued to flow from central banks, the global economy staged a recovery that was unusual for its length but also for its frustratingly slow pace of growth and for how few nations were allowed to suffer a moment’s pain. In 2017—many years into its recovery—the U.S. pushed through a large tax cut to stimulate growth.

By 2019, only 7% of the nearly 200 economies tracked by the International Monetary Fund were in recession, and only 3% were expected to fall into recession in 2020—near a record low. As governments stepped in to do whatever it took to eliminate recessions, downturns no longer purged the economy of inefficient companies, and recoveries have grown weaker and weaker, with lower productivity growth.

What has happened during the pandemic is the story of the last four decades, telescoped into a matter of weeks and magnified to previously unimaginable scale.

Four months after the market crashed amid warnings that lockdowns would trigger another Great Depression, governments have intervened as never before. Many rich countries have rolled out stimulus measures amounting to 10% of GDP or more. That means an even bigger role for government, which will have to be funded by more debt.

After the global financial crisis of 2008, households and financial firms in many capitalist countries felt pressure to restrain their borrowing. Governments did not. The world’s total debt burden plateaued at a historical high of 320% of global GDP by the end of 2019, but within that total, government debt rose most rapidly. Many economists swatted away concerns about higher government debt arguing that with interest rates so low the borrowing could be easily financed.

The problem is that growing government involvement in the economy typically leads to lower productivity and weaker growth. A 2011 European Central Bank working paper found a “significant negative effect” of bigger government on per capita GDP growth in a set of 108 countries over the previous four decades. A recent report from BCA Research found a similar link in 28 major developed economies, including the U.S., over the last two decades.

The idea of government as the balm for all crises is appealing in the short term, but it ignores the unintended consequences. Without entrepreneurial risk and creative destruction, capitalism doesn’t work. Disruption and regeneration, the heart of the system, grind to a halt. The deadwood never falls from the tree. The green shoots are nipped in the bud.

Low interest rates are supposed to encourage investment in companies large and small, increasing productivity and boosting growth. Instead, as a recent paper from the National Bureau of Economic Research shows, low rates gave big companies a strategic incentive to grow even bigger, in large part because securing a dominant position in the market promises outsize financial rewards.

The big were growing bigger for many reasons, of course. The rise of the internet created a winner-take-all market, in which dominant giants could reach every consumer on the planet. Government regulations, which expanded at an accelerating rate over the past four decades, created a thicket of rules best navigated by big companies with armies of lobbyists and lawyers.

The big tech companies, in particular, came to sit on tens of billions in cash, much of which they used to buy back their own stock—hardly a productive investment in the future of the economy. As the large grew increasingly entrenched, they sucked up talent and resources, crowding out the little guys.

Startups represent a declining share of all companies in the U.S. and many other industrialized economies. Before the pandemic, the U.S. was generating startups—and shutting down established companies—at the slowest rates since at least the 1970s. The number of publicly traded U.S. companies had fallen by nearly half, to around 4,400, since the peak in 1996. And many of them started running up massive debts, in part as a desperate effort to grow in the shadow of the giants.

Today an astonishing number of the survivors are, quite literally, creatures of credit. In the 1980s, only 2% of publicly traded companies in the U.S. were considered “zombies,” a term used by the Bank for International Settlements (BIS) for companies that, over the previous three years, had not earned enough profit to make even the interest payments on their debt. The zombie minority started to grow rapidly in the early 2000s, and by the eve of the pandemic, accounted for 19% of U.S.-listed companies. Zombies are also spreading in Europe, China and of course Japan, where this phenomenon first became apparent.

With every crisis, more of these creatures of debt survive. Since the 1980s, recent Deutsche Bank research shows, each new U.S. recession has been met with more bailouts and easy money, leading to a lower rate of corporate defaults. Over the last 20 years, the falling default rate has also closely mirrored the slowdown in U.S. productivity, which is not surprising.

Keeping profitless companies alive naturally retards productivity. A 2017 OECD study found, for example, that “zombie congestion” in any industry lowers the productivity of rival companies—and blocks the entry of new companies—by raising labor costs and making it difficult to attract capital. Now forecasters expect companies with junk debt ratings to default at a rate of around 10% during the pandemic—a rate lower than in recent recessions, despite the historic depth and speed of the current contraction.

As lockdowns began in March, the Fed promised to start buying debt at a rate up to twice as fast as in 2008, including corporate bonds for the first time. Gradually, the Fed has loosened the definition of what it will buy. Even after the credit markets had settled down in June, the Fed ramped up purchases, and it now owns debt issued by, among others, Apple, Walmart,AT&T,Disney,Nike and Berkshire Hathaway.